The ECB is stuck between a rock and a hard place

The ECB is stuck between a rock and a hard place

Escalating sanctions will both lift inflationary pressures and weaken growth in the Euro Area

Given the macroeconomic economic shock imparted by the ongoing war in Ukraine, it is important to flag the potential fallouts and policy mistakes. I have flagged in my last note the importance of the sanctions on the Russian Central Bank, their short-term consequences for Russia’s financial stability and their long-lasting effect on the organisation of the international monetary system (I will write more on this soon).

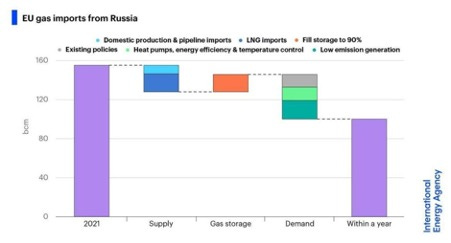

What now matters greatly is the EU’s ability to reduce the flow of hard currency to Russia and that means cutting energy imports and potentially rationing energy consumption in Europe soon. Bruegel has produced a remarkable piece about the ways and means to cut Russian energy dependency within a year, which relies heavily on LNG and on coal. The IEA has offered a 10 points plan for cutting Europe’s gas imports by 30%.

The US is also considering a proper embargo on Russian oil and gas, including possibly via secondary sanctions, which could be major and will have important implications for the oil markets as well as for geopolitics (Warming up with Iran and Venezuela for example).

In Europe, nobody has made the case for real rationing to reduce demand sharply. The European Commission is preparing a Communication that will be issued on Wednesday and that should lay out a few immediate steps that could be taken (possibly as early as Thursday/Friday when the European Council meets in Versailles).

Any such steps would have severe macro consequences for the European economy and should be taken into consideration when the ECB meets on Thursday March 10th. This was already poised to be a critical meeting as the ECB had announced its new forecast could lead to a more rapid normalisation, but it is taking a whole new dimension given the ongoing crisis and its likely economic fallout.

Indeed, it is likely that the governing council will be even more divided given the conflicting views and dynamics at play. Headline inflation risk is liable to increase sharply as supply side disruptions, sanctions and possible rationing push energy and key agricultural commodities’ prices higher. This will undoubtedly push the inflation forecast to be released by the ECB staff higher for longer, optically allowing the ECB to announce that all necessary conditions for the normalisation of its policy are now in place.

The reality is that the growth shock to be expected if Europe does escalate sanctions further and in particular if it takes aggressive steps to reduce its energy consumption and Russian oil & gas imports is going to be extremely significant and, in every way, comparable to the sort of partial shutdown of the economy that we experienced under COVID. There is therefore a clearly visible trade-off between the ECB’s inflation target and its support for growth and the general policies of the union (its secondary objective) and the governing council will be facing this trade-off head-on on March 10th.

There are indications that the Executive Board, let alone the Governing Council, is not unanimous and given the set-up and the build-up in expectations. It will be hard to kick the can down the road:

· On February 24th, on the day of the Ukraine, invasion Isabel Schnabel pronounced a particularly hawkish speech about inflation risk and defended the normalisation sequence as being both appropriate and flexible enough. This speech is probably not going to age well.

· On February 28 Fabio Panetta has rightly insisted that while inflation risks were serious, they were mostly imported and had not fed an increase in inflation expectations (if anything inflation expectations are down sharply since the Russian invasion on February 24th). He therefore made a bold call for prudence given the prevailing uncertainty but also, unlike Isabel Schnabel, clearly opened the question of the sequencing of the normalisation and stressed the fact that in the absence of a clear framework, it could pose risks to financial stability and fragmentation.

· Philip Lane followed on March 2nd with a speech that tries to provide a form of synthesis that places the ECB’s action back in the context of the monetary policy strategy framework agreed with the last review and effectively stressing the: “the importance of monitoring the transmission mechanism in calibrating monetary policy instruments and the recognition that financial stability is a precondition for price stability”. But he seems to be of the view, like Schnabel, that the policy announced at the December 2021 meeting provides enough flexibility, in particular the reinvestment policy of the PEPP and PSPP programme.

Conclusion

§ All in all, the ECB must accept that it will be facing higher inflation for longer, that this inflation shock is largely exogenous and unlikely to feed domestic inflationary dynamics given the ongoing economic fallouts of the war in Ukraine.

§ The central question is how it will respond to a potential adjustment in the exchange rate and its impact on the normalisation sequencing. Keeping asset purchases in play for longer seems necessary, especially given the expected fiscal consequences of the war.

§ Some are also arguing that in the event of real sell-off in the EUR, the ECB could step in via interventions. This seems unwarranted and unlikely given the real effective exchange rate of the EURUSD (fairly strong by historical standard, in keeping with the Euro Area considerable current account surplus) offers ample space for adjustment.