Has the ECB just ended its implicit "spread control" framework?

The decision to phase out the PEPP and reduce the pace of purchases under the APP might be more important than meets the eye

The ECB’s meeting last week was probably more important than meets the eye. Indeed, while it had already largely telegraphed the decision to phase out its Pandemic Emergency Programme (PEPP), the flexibility around the decision and the extent to which the other Asset Purchase Programme could take over was unclear.

The ECB essentially announced that:

Asset purchases

§ Net asset purchases under the PEPP will be implemented at a lower pace in Q1 2022 than in the previous quarter and it will be discontinued entirely at the end of March 2022.

§ In the event of renewed market fragmentation related to the pandemic, PEPP reinvestments can be adjusted flexibly across time, asset classes and jurisdictions at any time. This could include purchasing bonds issued by Greece to avoid an interruption of purchases in that country.

§ The APP monthly net purchase pace will gradually go down through 2022 from €40 billion in the second quarter and €30 billion in the third quarter under the APP. From October 2022 onwards, the Governing Council will maintain net asset purchases under the APP at a monthly pace of €20 billion for as long as necessary to maintain the accommodative impact of its policy rates.

Reinvestment policy

§ It will reinvest the principal payments from maturing securities purchased under the PEPP until at least the end of 2024, thereby extending the reinvestment horizon.

§ It will continue reinvesting, in full, the principal payments from maturing securities purchased under the APP for an extended period past the date when it starts raising the key ECB interest rates, as already committed.

Long Term Refinancing Operations

§ The ECB will assess how targeted lending operations are contributing to its monetary policy stance.

§ the special conditions applicable under Targeted Long Terme Refinancing Operations III will end in June next year.

§ It will assess the appropriate calibration of its two-tier system for reserve remuneration so that the negative interest rate policy does not limit banks’ intermediation capacity in an environment of ample excess liquidity.

All in all, the ECB is doing both normalizing its policy because the acute stress related to COVID is gone but also signalling greater concerns over inflation in its forecast. This helps to see the normalization as broader than just ending the PEPP and is confirmed by the commitment to reduce the size of the APP over 2022.

While the decision to end net asset purchases under the PEPP was expected, what is more surprising is the numerical commitment on the APP through 2022. Indeed, many hoped that the APP could essentially inherit the flexibility given the PEPP. The numerical commitment made towards monthly purchases being gradually reduced every quarter through to the end of 2022 will limit the flexibility of the ECB to adjust.

The ECB has softened the edge of this decision by offering a more generous reinvestment policy for the PEPP. The PEPP reinvestment policy (full reinvestment extended until 2024) together with the PSPP reinvestment policy ensure together that the balance sheet of the ECB will keep growing (excluding TLTRO repayments).

The flexibility in the reinvestment policy will allow in practice to keep buying some Greek bonds (Greece is eligible to the PEPP but not yet to the PSPP), but this may prove insufficient. The ECB’s policy however does open the door to flexible reinvestment of the PEPP roll-overs, therefore paving the way for potential meaningful divergence from the capital key distribution over time.

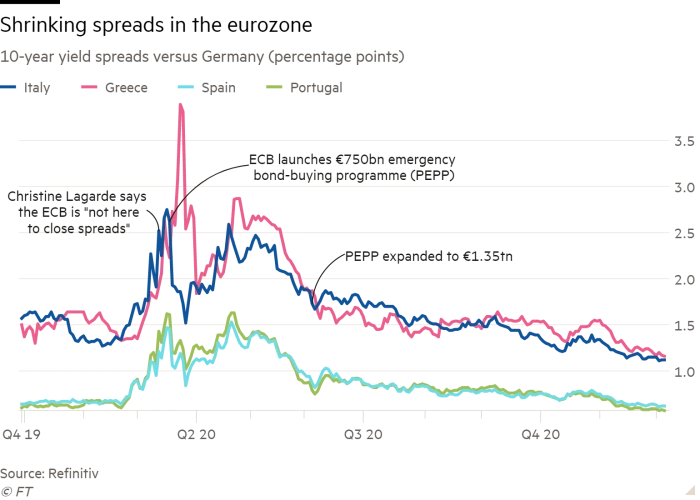

In practice however, the flexibility of reinvestment under the PEPP may prove insufficient to stabilize spreads in other jurisdictions. The PEPP had introduced a de facto “spread control” framework in Europe. Its unwinding is a real regime shift. The fact that the ECB is ending its de facto spread control framework is likely to be tested by markets. With this new framework, in 2022 the ECB will buy about 80% of the euro area government bond supply (down from 125% in 2020-21) and 70% for Italy (down from 120% in 2020-21).

Beyond the single largest upside revision to the inflation forecast, this decision may lead to question whether the chosen normalization sequence is the right one for Europe. Indeed, it might be that the financial and monetary conditions in Europe are more heavily directed by long term spreads than they are by short term rates.

If that were the case, that would argue for a different normalization sequence in the Euro Area: normalizing rates first and keeping generous and flexible buying to anchor spreads.

Chart: Courtesy of Ducrozet (Pictet)